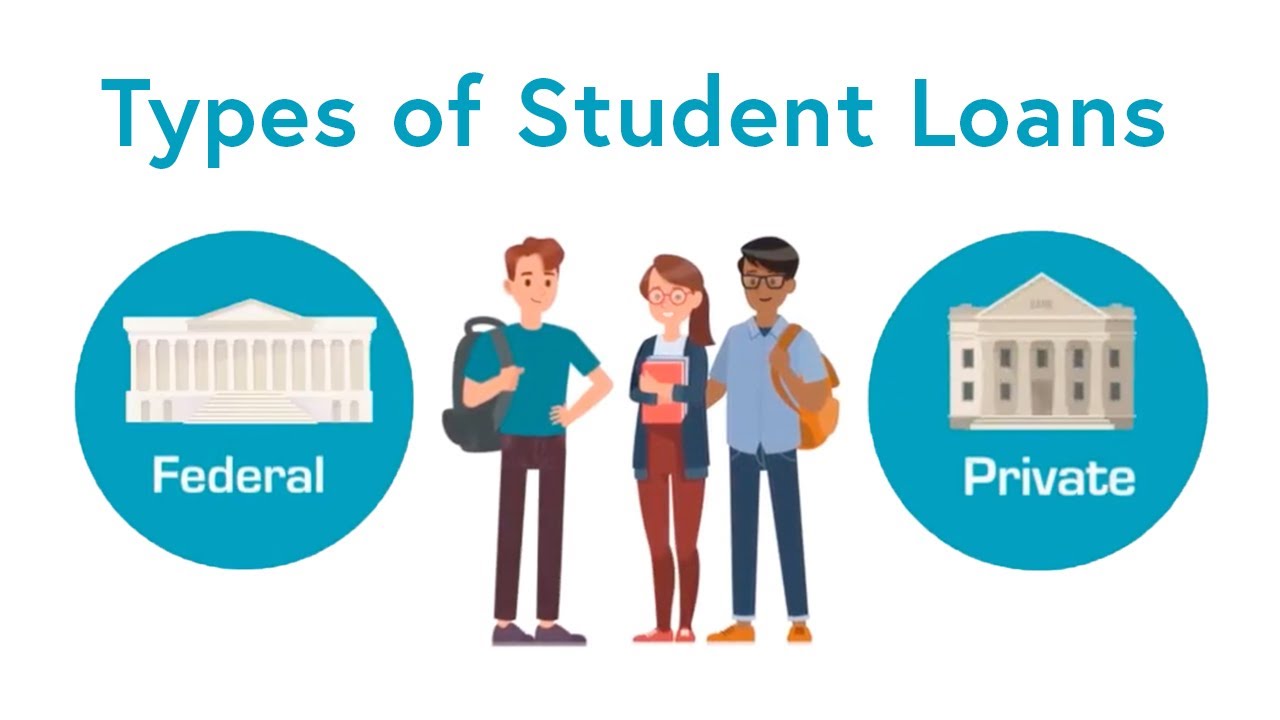

Types of Student Loans

One of the main elements of preparing for college is putting your finances in order to pay for college tuition and manage other personal expenses. Students pay for college using federal grants, scholarships, work-study, college savings, payment plan, and students loans or a combination of either.

For students exploring the loan options, there are several loan options to explore from. The various loan options are broadly categorized into federal student loans and private student loans.

What are Federal Student Loans?

A federal student loan is a loan that’s offered by the U.S. Department of Education to help pay for college or career school.

They come with a lower interest rate and more accommodative repayment terms. Student need to submit the government’s Free Application for Federal Student Aid (FAFSA) to qualify for federal loans.

There are a couple of details collected from the student during student loan application ranging from student’s and parent’s income and investments, to matters touching on the whole family including other college-attending siblings. During application, the data collected helps to draw up a student’s financial profile that qualifies them to a certain amount of federal funding package

What are the different types of Federal Student Loans?

Direct Subsidized Loans

For undergraduate students with financial need, these loans don’t accrue interest while the student is in school at least half-time, during the six-month grace period after graduation, and during periods of deferment (postponement of loan payments).

The loans are offered to students based on their established financial needs and come with subsidized interest rates.

Direct Unsubsidized Loans

For undergraduate and graduate students; there’s no need to demonstrate financial need to qualify. Interest accrues on unsubsidized loans from the time the loan is disbursed until it’s paid in full.

The unsubsidized loans are not based on the student’s financial needs but the student is fully responsible for paying the interest on the loan while in school and during grace periods or deferment/forbearance.

Direct PLUS Loans

For graduate students and parents of dependent undergraduate students; creditworthy borrowers can get this loan to help pay education expenses not covered by other financial aid.

The Direct PLUS Loan for graduate and professional students has a higher interest rate than Direct Subsidized and Unsubsidized Loans but comes with the same repayment terms.

Direct Consolidation Loans

For anyone with multiple federal student loans, this program allows you to combine all your federal student loans into a single loan with one monthly payment.

What are Private Student Loans?

A private student loan is a non-federal loan made by a lender such as a bank, credit union, state agency, or a school. They often come with higher interest rates and less flexible repayment terms than federal loans.

Eligibility for most private student loans is based on the borrower’s—and sometimes a co-signer’s—credit history, rather than financial need. Private student loans can be used for various purposes including paying tuition, room and board, fees, book, supplies, transportation, and computer for school to name a few.

Who offers Private Student Loans?

Banks, financial institutions, state agencies, and schools offer private student loans based on the student’s credit worthiness. The process takes into account both the student’s and the cosigner’s credit plus other detailed provided during student loan application.

Repayment Options for Private Student Loans

There are several repayment option available for private student loans which may include:

Deferred Repayment

You don’t have to make payments on the principal while you’re in school. But, interest will accrue and be added to your principal balance. When you enter repayment, your monthly payments will be higher because you’ll be paying off the accrued interest plus the principal.

Interest-Only Repayment

You make low, interest-only payments while you’re in school. This option can help keep your loan balance from growing during deferment or forbearance; however, when you enter repayment, your monthly payments will be higher because you’ll be paying off the accrued interest plus the principal.

Full Principal and Interest Repayment

You make full monthly payments on the interest and principal while you’re in school. This option may help you pay off your loan faster, but your monthly payments will be higher than with other repayment plans.

How to compare private student loans?

There are a few things to compare when taking out a private student loan:

Loan Term

The number of years you have to repay your loan. A longer loan term will mean lower monthly payments, but you’ll pay more in interest over the life of the loan. A shorter loan term will mean higher monthly payments, but you’ll pay less in interest over the life of the loan.

Fixed or Variable Interest Rate

A fixed interest rate won’t change over the life of your loan, so your monthly payments will stay the same. A variable interest rate may start out lower than a fixed rate, but it could increase over time.

Loan Fees

Some lenders charge fees, such as an origination fee, which can add to the cost of your loan.

Repayment Options

Some lenders offer repayment options that can help make your loan more affordable, such as interest-only payments or deferring payments while you’re in school.

Prepayment Penalty

Some lenders charge a penalty if you pay off your loan early.

Cosigner

Some lenders require a cosigner, while others allow you to apply with a co-borrower.

Types of Private Student Loans

There are two types of private student loans:

Secured Private Student Loans

A secured loan is one that requires collateral. The collateral is usually in the form of property, such as a car or home.

Unsecured Private Student Loans

An unsecured loan does not require collateral and is based on the borrower’s creditworthiness.

How to Apply for a Private Student Loan?

The first step is to fill out a Free Application for Federal Student Aid (FAFSA®) form to see if you’re eligible for federal student aid.

If you’re not eligible for federal student aid or you need additional funding, you may want to consider a private student loan.

To apply for a private student loan, contact the lender of your choice and complete their application process.

Not all lenders require a co-signer, but having one may help you get a lower interest rate.

If you’re approved for a loan, the lender will send the money directly to your school to pay for your education-related expenses.

Conclusion

There are several types of student loans available to help pay for college, including federal student loans and private student loans.

Each type of loan has its own terms and conditions, so it’s important to compare the different options before you decide which one is right for you.

Applying for a private student loan is simple and can be done directly through the lender of your choice. Be sure to shop around and compare different lenders to find the best loan for you.